Three companies. Four trillion dollars of combined valuation. One question nobody has asked: Would they pass a credit check?

4D Contact, Global Debt Recovery and Credit Management ServicesWritten by Martin Kirby

Read it in 6 minutes

1200

627

1200

627

Written by Martin Kirby

Read it in 6 minutes

Martin Kirby

Martin has worked within credit and risk for over 30 years, holding senior positions at organisations such as Business Stream, Kier Group, Adecco UK, and Bupa Healthcare. Martin’s exceptional leadership has earned him industry accolades, including Credit Manager of the Year and Corporate Credit Team of the Year. Martin holds an MBA from INSEAD, providing him with a global perspective on strategic finance, change leadership, and innovation.

17 June 2026

As Credit Directors, we spend our careers assessing businesses on a fundamentally simple question: if we extend credit, will we get paid?

Yet in today’s stock market, some of the world’s most valuable companies are being evaluated almost exclusively through the lens of growth, innovation, and investor sentiment. Businesses such as OpenAI, SpaceX and Anthropic command valuations measured in trillions of dollars, attract unprecedented levels of investment, and dominate headlines around artificial intelligence and technological disruption.

But valuation and creditworthiness are very different things.

In this article, while investors around the world prepare to speculate on these businesses, we assess them through a different lens: that of the credit professional. Looking beyond the market hype, we examine how OpenAI, SpaceX, and Anthropic perform against traditional measures of credit risk, cash generation, profitability, governance, and payment capacity. If these companies were applying for a trade credit account rather than preparing for a public listing, would they satisfy the same due diligence and credit assessment criteria applied to any other customer?

Three companies are preparing to go public at a combined valuation somewhere north of $4 trillion. The coverage so far has asked one question: should you buy the stock?

I have spent forty years asking a different one. If these businesses walked through my door asking for a trade credit line, what would I grant them?

So I ran the exercise. I took the IPO class of 2026 – OpenAI, SpaceX, Anthropic – and put each of them through the same assessment I would apply to any new account application. Same pillars, same discipline, same scepticism. Financial strength, cash generation, ownership and control, group structure, payment capacity, and the question that sits underneath all of them: where does the money to pay me actually come from?

The results were instructive.

A quick note before we start – this is a thought experiment, not investment advice. The figures below are as reported in recent coverage and filings. Please treat the numbers as directional. The method, however, is exactly what I would do on a Monday morning.

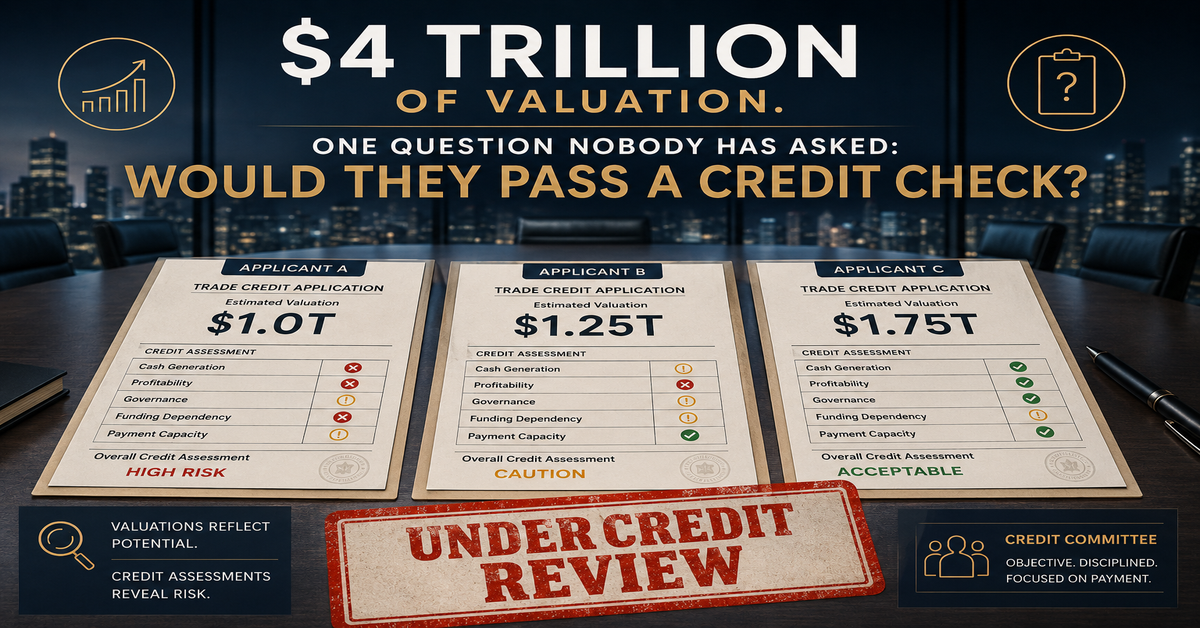

The numbers on the form. Roughly $2 billion a month in revenue. Projected losses of $14 billion in 2026. Seeking a public valuation around a trillion dollars.

The credit manager’s read. Revenue of this scale is genuinely impressive – there are FTSE 100 businesses that would trade their grandmothers for $24 billion a year. But a credit assessment does not reward revenue. It rewards the ability to convert revenue into cash that pays creditors. A business projecting a $14 billion loss is, by definition, consuming someone else’s money to operate. Today that someone is venture capital and sovereign wealth. Tomorrow it is the public market. At no point in that chain is it the customer.

When I see a debtor whose operating model depends on continuous external funding, I ask one question: what happens to my invoice if the funding pauses? The honest answer here is that nobody knows, because the model has never been tested without the tap running.

Verdict: Decline open terms. Proforma or secured only. Magnificent business. Not yet a creditworthy one.

The numbers on the form. Preparing to list at $1.75 trillion. One genuinely profitable division – Starlink, reported at $4.4 billion operating profit in 2025. A rocket programme that has completed twelve test flights without delivering a commercial payload. An AI business reported to have lost more than $6 billion last year. One shareholder retaining 85.1% of voting rights.

The credit manager’s read. This is the classic group-structure problem, and any credit professional who has worked construction or logistics has seen it a hundred times at smaller scale. One profitable entity quietly carrying the rest of the family. The assessment question is never “is the group impressive?” It is “which entity is my counterparty, and does the profit sit there?”

If you contract with the profitable bit, fine. If you contract with the group, you are exposed to every loss-making sibling in the bundle – and to a concentration of control that means strategy can change overnight with no recourse. An 85.1% voting block is not a governance footnote. In credit terms it is key-person risk with a market cap.

Verdict: Conditional approval – Starlink entity only, modest limit, parent guarantee declined as worthless on these terms. You cannot guarantee yourself.

The numbers on the form. First operating profit, reported at roughly half a billion dollars. Valuation near $1 trillion, having more than doubled between February and May.

The credit manager’s read. The only application in the pile with the line every credit manager actually wants to see: more money came in than went out. That matters. Profitability, even modest profitability, changes the character of a debtor entirely. It means the business can, in principle, pay you from trading rather than from fundraising.

But then there is the valuation. A doubling in three months is not a trading signal; it is a sentiment signal. And sentiment is the most volatile security on earth. My job is not to assess what investors believe. It is to assess whether the cash keeps arriving when they stop believing. Half a billion of operating profit against a trillion of expectation is a thin cushion if the mood turns.

Verdict: Approve. Modest limit, monthly review, watch the burn. The only one of the three I would trade with on open terms – carefully.

The public market is about to do what no credit committee on earth would do: grant these three businesses combined limits in the trillions, unsecured, with no payment terms, no retention of title and no right of recall.

That is not a criticism of the companies. It is an observation about the difference between investing and underwriting. Investors are paid to imagine the next decade. Credit managers are paid to ask about the next ninety days. Both disciplines are legitimate. Only one of them is currently being applied to these valuations.

The practical conclusion for those of us who run ledgers rather than portfolios: the products these companies sell are currently priced below what they cost to provide, subsidised by investors who need a story to exit into. That subsidy is real, it is generous, and it has an expiry date.

So use the product. Build the capability while the pricing lasts. And keep doing what we have always done – judge every counterparty not by what the market says they are worth, but by whether the cash actually arrives.

The market values these businesses in trillions. I would start them on thirty days, modest limits, and a review in ninety.

Some habits are worth keeping.

Martin Kirby FCIM

(Credit to Richard Owen, whose recent piece on the economics of this IPO cycle prompted the exercise.)

Is your business looking to improve it’s financial position?

4D Contact provide a comprehensive suite of global outsourced credit-control and debt recovery services for businesses looking to improve cash collection and build resilience and financial stability:

Contact us now at sales@4dcontact.com or +44 (0)20 3773 7854

![[TOFU offer] eBook – A C-Suite executive’s guide to Delivering successful order-to-cash transformation](https://www.4dcontact.com/wp-content/uploads/2019/08/img-ebook-preview-order-cash-transformation.png)

A review of the considerations and tactics critical to achieving successful transformation within your order-to-cash function

Download free guide